A review of 2024's over-engineered predictions and a view into 2025

I’m very late to the party in wrapping my fintech takes from 2024 (I was a bit preoccupied with locking down my dream job at Cash App after my third application) but I’m finally getting around to reflecting on 2024 with a quick view into 2025.

Here’s what I predicted would happen in January 2024:

Stripe IPO mid 2024 with mid-teens IPO pop

Fintech AI use case finally launches - generative AI CX chatbots to replace IVR & email

Varo runs out of cash and is acquired by regional bank or fintech looking to buy charter

Risk/AML/KYC fintech with ~$1bn+ valuation (in 2021) acquired by larger fintech

Merger / competitive takeout of 1-2 BaaS players

Consumer credit fintech starts to have its neobank, BNPL hype moment

FedNow doesn't materially change anything for banks / fintechs

Let’s take an over-engineered fintech deep dive to see how I fared.

(Spoiler alert - I got 80% of these correct, and I’m up to 93% if you count the first two months of 2025!).

1/ Stripe IPO mid 2024 with mid-teens IPO pop

Realized: February 2024 (Partially)

I’ll admit that this wasn’t necessarily a hot take as every fintech nerd has been predicting this one for quite a while now, but I do think it was impressive how quickly it nearly came true. Okay, their tender offer wasn’t quite an IPO, but almost all the other elements were basically true about this prediction! Announced in February 2024, they raised money by April 2024 (close enough to mid 2024) and ended up raising ~$700M alongside a moderate valuation pop (30% feels close enough to mid teens right?). It wasn’t quite the IPO everyone was hoping for, but it still gave employees some much needed liquidity and reset expectations on valuation.

I’ll give myself a 50% score on this one. 0.5 / 1.

2/ Fintech AI use case finally launches - generative AI CX chatbots to replace IVR & email

Realized: February 2024

This prediction felt like a bigger call at the time because when Klarna announced that its AI assistant was already solving ~70% of support conversations which was equivalent to the work of 700 full-time agents which in turn was saving the company $40M in profits, the world was understandably blown away. Sebastian got some flak for what was seen as a tone-deaf post in the face of increasing fears about AI taking human jobs (which by the way, I disagree with as he clearly asks important questions about the impact AI may have on society). But no matter whether you agreed with it or not, the update caused ripples across the fintech ecosystem and the business industry more broadly, as it was the first material in-production AI investment that changed business trajectory.

With all that said, I felt like I had a bit of a cheat code on this, because we had already been pursuing initiatives like this at Chime since at least 2019. I remember working closely with our CX PMs to price out and ultimately deploy an AI-powered chatbot alongside a revamped robo-IVR that increased our containment rates (the percentage of interactions solved by automated sources) by 30%+. Like Klarna, we not only saw massive cost savings but also an improvement to customer NPS, all the while freeing up agents to work on more difficult customer service issues that required human interaction (so a win-win-win). It’s a reminder that AI isn’t new, just our interaction layer (the innovation of ChatGPT isn’t the tech, it’s the chat interface).

In any case, this felt like a spot on prediction so +1 for me. 1.5/2 so far.

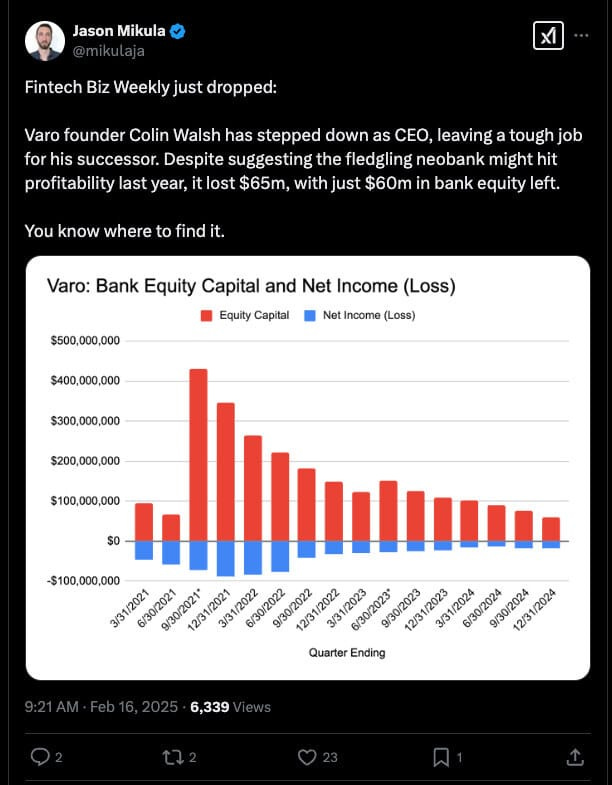

3/ Varo runs out of cash and is acquired by regional bank or fintech looking to buy charter

Realized: Not realized

My first full swing and a miss here. Not only did Varo not run out of cash, it trimmed its losses and as of September 2024 seems on track for profitability (did they see my tweet and accept the challenge?). They reduced marketing spend by 85% from its peak, introduced new products like Smart Bank Account for PFM and a Line of Credit product. And they inked a deal with Marqeta

I’ve got to say I’m both not proud of this prediction and very happy I was incorrect here. It was not part of my otherwise optimistic spirit for fintech in general and didn’t give Varo the benefit of the doubt in terms of how it would continue to develop. I’m just generally of the mind that most fintechs don’t need a bank charter to be successful and spending $100M+ and 3 years to get one hasn’t done Varo any more favors relatively than other fintechs on similar footing. But all power to them for being the first challenger bank to get one (SoFi’s was through an acquisition and Block’s is an ILC). And all kudos to them for hanging in there.

All that said, as of February 2025 (so it’s good to procrastinate!), it looks like some part of my prediction may be coming true as reports indicate that Founder and CEO Colin Walsh may be stepping down as equity capital continues to dwindle.

But as of the end of 2024, I’m bageling it with a 0. Running total 1.5/3.

4/ Risk/AML/KYC fintech with ~$1bn+ valuation (in 2021) acquired by larger fintech

Realized: September 2024

2024 was a big year for Risk fintech M&A - Upay acquired AML solutions platform AML Go and Socure paid $140M to acquire AI risk decisioning platform Effectiv. But the big deal that realized my prediction was Visa’s nearly ~$900M acquisition of Featurespace, a UK-based enterprise fraud management and AML vendor employing more than 400 people. Forrester believed the acquisition would further expand Cybersource’s AML solutions and provide more issuer-facing and ecommerce-facing fraud management tools.

I’ll admit though, that the specificity of this prediction came not from an expectation of a Visa acquisition but rather from a large consumer fintech like Block or Chime buying out a premier risk vendor like Socure. Socure last raised a massive $450M round in 2021 valuing the company at $4.5B and while that valuation may have signaled a peak valuation, I was sure that someone might want to pick them up to consolidate risk tooling and potentially hold back the competition by in-sourcing a key platform vendor. While that didn’t come into play, I’m sure we’ll see more M&A in this space in 2025.

We’ll take the W here though. 2.5/4 at this point.

5/ Merger / competitive takeout of 1-2 BaaS players

Realized: April 2024 (and then unrealized May 2024)

You couldn’t get away from the talk of “Synapse” in 2024 - it was fintech’s biggest drama and it snowballed into something even mainstream media was covering. There’s so many layers to this story, but let me try to summarize:

In August 2022, Evolve announces they are ending their relationship with BaaS provider Synapse amid a messy lawsuit around an allegedly missing $14M.

In September 2023, Mercury, Synapse’s largest client, announces an end to their relationship and moves to a direct relationship with the underlying sponsor bank Evolve. Later Mercury filed a $30M lawsuit against Synapse to support the ongoing arbitration process between the two parties.

In October 2023 Synapse hit by “macroeconomic conditions” and lays off 40% of its workforce, amid the growing fallout over Mercury’s departure.

By April 2024, the a16z-backed Synapse files for Chapter 11 bankruptcy, throwing 100 direct business relationships and ~10M+ retail customer relationships into a state of confusion.

Two days later, Tabapay, the instant money movement platform backed by Softbank, announces plans to acquire the assets of Synapse for ~$10M - saying that Synapse’s assets would be a “great natural fit” and they would grow its offerings “in tandem with providing continuity to Synapse clients and banks.” Meanwhile, Synapse assured clients that there will be “no immediate changes in operational processes or to your business model.”

But two weeks later in May 2024, it became clear that the white knight moment wasn’t meant to be. Tabapay abandoned plans to purchase the assets of Synapse, purportedly because Synapse could not fulfill a closing condition that would ensure that all FBO accounts held at Evolve would be fully funded at close. At that time, the gap was thought to be ~$50M

By mid-May 2024, as Synapse proceeded with its bankruptcy, some 100K customers encompassing $265M in deposits across fintechs like Yotta, Juno and others were locked out of their accounts. The FDIC also reminded folks that the failure of nonbanks won’t trigger FDIC insurance, only adding to the furor.

By June 2024, the fallout expands to the mainstream as new indications are that the asset shortfall is up to $96M vs. the $50M initially estimated and former FDIC chair, Jelena McWilliams, appointed as trustee to oversee the bankruptcy says that finding all customer money may be impossible.

As of November 2024, the fate of ~$70M+ in customer funds is still unclear as the different counterparties throw their version of events into the public forum. In a detailed post, Evolve reaffirmed that it has completed its side of the reconciliation process having returned ~$25M+ in funds already as of November 2023. Meanwhile, trustee McWilliams suggests via a November court filing that Synapse may not have been performing any daily reconciliations of balances for some time. Yotta, Juno (of which I’m an angel investor) and other fintechs continue to fight for customer funds, but the situation isn’t looking too bright.

Of course, BaaS had a rough go of it in 2024 as regulatory dynamics and continued questions about product-market-fit came to a boiling point. Per Techcrunch:

The banking-as-a-service space as a whole has faced turbulence in recent times. Several players in the industry have announced layoffs over the past year. Most recently, Synctera cut about 15% of its staff. Treasury Prime slashed half its 100-person staff in February, a year after it announced a $40 million Series C raise. Figure Technologies, which includes Figure Pay, laid off 90 people — or about 20% of its workforce — last July. Meanwhile, Piermont Bank recently reportedly cut ties with startup Unit, Fintech Business Weekly reported.

The crisis only further accelerated regulatory crackdown and has put a glaring question mark around the efficacy of the partner bank model and the omnibus FBO account ledgering process writ large (a model that’s used by fintechs from Block to PayPal to Chime).

I’m hopeful this story turns around as I’m a long-term supporter of BaaS and think highly of the compliance-focused and high product velocity players in the mix, including my alma mater, Unit. It does seem like 2025 may be a turning point, but I wouldn’t be surprised if a few mergers, fire sales or acquisitions that couldn’t get done in 2024 roll into the early part of 2025.

I’ll take the credit on this one, but its with a heavy heart. 3.5/5.

6/ Consumer credit fintech starts to have its neobank, BNPL hype moment

Realized: June 2024

The drama kept coming in 2024 when in June 2024, the WSJ reported that Wells Fargo was losing millions of dollars per month on its partnership with breakout fintech, Bilt Rewards (which was giving folks 1% rewards on rent payments) and it again turned our ecosystem on its head. The gist of the argument was the following (as summarized perfectly by Sheel Mohnot on X):

Wells Fargo assumed that the Bilt card would be the top of wallet card for renters who carry balances but instead most users just use it for rent + 5 required transactions

Wells Fargo assumed that 65% of card purchase volumes would be non-rent which would generate interchange revenue but the reality was it was 65%+ rent-related which earn very little interchange (<40bps gross and effectively negative when factoring in cashback)

Wells Fargo assumed 50-75% of balances would be revolving which would earn interest but the reality is most don’t carry a balance and only 15-25% is revolving

Wells Fargo is paying ~0.80% to Bilt on rent payments and was hoping to cross-sell its mortgages but that hasn’t happened yet

For what it’s worth, I personally think the early takes that the WSJ somehow exposed that the cash back on rent payments model doesn’t work are just plain wrong and it helps that both WF and Bilt denied that there are issues in the contract and notably it extends until 2029. I also find it funny that a WSJ reporter talked to only Wells Fargo about the contract negotiation and seemed to take at their word opinions that could just as easily have been actual talking points during a negotiation (didn’t they wonder why WF was so eager to “leak” this to the press?).

There’s likely a bigger post coming on this, but here’s a few counterpoints to the main points of the article to start:

We are literally 2 years into a 7 year partnership. It’s way way too early to measure top of wallet success. Any increase in spending would be considered a success here and let’s not forget that they have the actual rent payment on the card (if rent isn’t your biggest monthly spend, I want to be you)

There is no way that Wells Fargo actually thought this and I’m sure the statement was misinterpreted. I think what was actually said was 65% of non-rent card purchase volumes would not related to rent-related payments (e.g. utilities, maintenance, internet) and it was misstated here. I think Wells Fargo was well aware that the vast majority of spend on the card would be rent-related as that’s the case for every individual anyway (~50%+ spent on rent/housing-related payments). People were so eager to dunk on Bilt they had to assume Wells Fargo was stupid, but remember the age-old axiom “Banks are slow, not stupid.”

I cannot believe that this was true either and think this is another misinterpretation (actual statement was probably 50-75% of non-rent payments would revolve). It’s well known that for the credit score that Bilt was targeting the revolving balance is only 20-30% or less. Getting to 50-75% would mean they’re either targeting subprime creditors which aren’t eligble for the card (<580) OR they assume that the core demo somehow can revolve on rent payments (which isn’t possible or this product wouldn’t exist)

Again, we are two years into a 7 year relationship. At the time of posting, Bilt didn’t even have an upsell motion for users that were looking to buy a home. Within months they launched a program to earn Bilt points on home purchases alongside revamped tools to help renters estimate monthly payments including taxes and insurance. This is just the tip of the iceberg and any smart fintech nerd can see a million ways to expand the upsell opportunities

Ultimately, the article hinged around a supposedly huge number of $10M / month in losses, but we’re talking about a bank that makes $20B per quarter - this is a rounding error. I don’t know if Bilt will succeed but I do think that judging them by this article is the wrong way to evaluate them.

And let’s not forget the famous quote from Jamie Dimon when remarking on the success of the Chase Sapphire Reserve Card:

One of the fictions here is that the marketing cost ... gets booked over 12 months. The benefit of the card gets booked over 7 years. The card was so successful it cost us $200 million, but we expect that to have a good return on it. I wish it was a $400 million loss

Jamie Dimon

If nothing else though, the article did help bring more interest to consumer credit in the mortgage space and we saw mortgage servicing platform Haven launch Haven Wallet in September 2024, Bilt competitor Mesa launch in November 2024 and Further announce its launch to help aspiring homeowners find homes.

Whether you love ‘em or hate ‘em, Bilt indeed launched the credit fintech hype moment (and helped make my prediction come true).

Full credit on consumer credit on this one! 4.5/6.

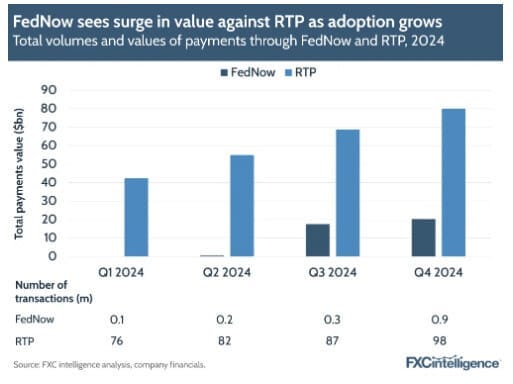

7/ FedNow doesn't materially change anything for banks / fintechs

In hindsight, this one may have felt easy to predict but at the end of 2023, there was far more hope for FedNow’s instant payment service. The real-time low-cost 24/7/265 payments system governed by the Federal Reserve was estimated to be “fully operational” by 2024 and instantaneous, low cost transactions were aimed to help mainstream Americans avoid overdraft and late fees often because of transaction settlement timing.

Ultimately the system launched in July 2023 with 35 participating institutions that quickly grew to 300 participating financial institutions by the end of December 2023 and given the progress, there were high hopes that this progress would continue and we’d see significant volume in 2024. The growth in institutions was also paired with some optimism around volume, with the separate but potentially related rise in pay-by-bank which was already 9% of ecommerce payments in 2022 and was forecast to grow by 14% per year through 2026, in part thanks to FedNow.

Alas in 2024, while there are now over 1,100 “participating institutions,” there are no real volumes to speak of and no material changes to the cost or speed of payments as a result. There have been reports of “millions of transactions” processed and a note of high performance and reliability but total volumes were only ~$20B in Q4-24, a drop in this trillion dollar market. And of course millions of transactions is just a fraction of the 98M+ processed by The Clearing House’s private competitor to FedNow, Real-Time Payments (RTP).

At first, the lack of progress is surprising given that 86% of businesses and 74% of consumers surveyed by the Fed said that they’ve used faster or instant payments in 2023. But as you deep dive, it’s clear there are some major issues holding FedNow back:

Only 40% of financial institutions who use FedNow have signed up to send payments, limiting the value of the 1,200 institutions on the platform (just a fraction of the 8000+ banks in the US)

FedNow has a transaction limit of $500K max whereas RTP is up to $10M (important for large institution adoption)

General consumer lack of awareness combined with gradual rollout procedures for financial institutions have prevented viral network effect loops from kicking off

Still, I’m hopeful that 2025 is the year for change. The Federal Reserve is introducing new pricing that lowers the costs of entry for smaller institutions which can enhance the network effect and indeed FedNow participating institutions are already about 2x as big as the RTP network (though 80% of participating institutions are credit unions and small banks). Combined with the fact that more institutions are going to be enabling “send payments mode” after trialing receiving payments in addition to a potential uptick from banks that are already making changes to adopt the new ISO20022 standards by March 2025, may signal bigger flow upticks.

So 2024 was indeed a year of failure, but perhaps a good setup for 2025. 5.5/7 = ~80% correct!

So what’s next for 2025?

With the much-needed overconfidence of beginner’s luck, let me put out another year of over-engineered fintech takes.

Here are my takes for 2025:

We see successful fintech IPOs from Chime, Klarna and Navan that bring back the fintech hype with double digit IPO price boosts

Robinhood is the first of the fintechs to launch AI-driven consumer fintech products among the currently public fintech companies

At least one major BaaS takeout and one major neobank acquisition in 2025 as we see more consolidation in the space

BNPL gets its credit moment as new fintech launches allow for credit reporting to agencies

FedNow is successful enough in 2025 that it starts publishing volume estimates as it passes $100B in processed volume

Keep me honest as we track these in 2025!