Charts & Tarts: Fintech Edition

5 charts on the future of fintech - Trends in stablecoins, card networks, bank branches, and revenue multiples

Today’s post is a guest post from my good friend, Charles Rubenfeld. Charles and I connected over a mutual love of fintech and he mentioned that in addition to being equally awesome himself, he writes a newsletter and hosts a periodic “Charts & Tarts” series where participants bring a chart about a topic and explain it to their peers, with access to tarts and pizza along the way. Charles has prior experience at Uber, Valon & Scale and is focusing on writing and consulting. Shoot me a note if you’re interested in catching up with Charles!

Fintech is back! We’ve seen big new funding rounds from startups like Ramp and Mercury, and rising public company valuations for Robinhood, Coinbase, Affirm, and more.

To celebrate, Samir and I brought together a group of fintech operators and VCs for this month’s Charts and Tarts to discuss interesting trends in the fintech space and what might happen next. Below are some charts shared at the event and a summary of the discussions we had.

And if you’re interested in the “Charts & Tarts” series, check out some of our other sessions:

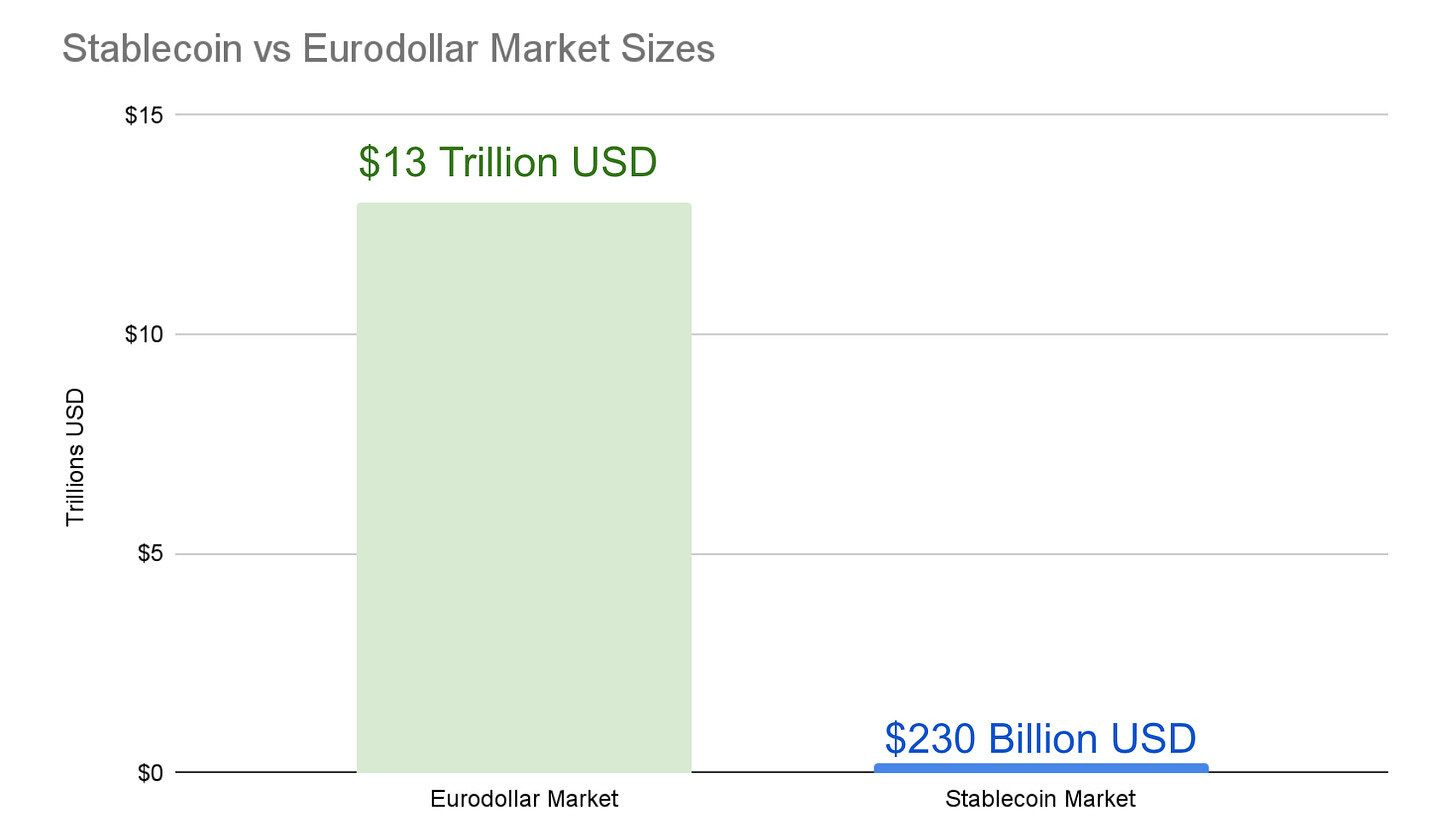

Stablecoins can take on the Eurodollar market

Sources: BIS for Eurodollar market, Stablecoin Market Caps

Stripe recently bought Bridge (a stablecoin API company) for $1b and described stablecoins as “room-temperature superconductors for financial services” in its latest annual letter.

In a world where crypto has struggled to find use cases1 , stablecoins have an obvious one: competing with the Eurodollar market. These are dollars held outside of the US (not necessarily in Europe, despite the name) that help facilitate offshore borrowing, lending, and transactions in US dollars. At nearly $13 trillion US dollars today, this market shows the massive demand to use dollars outside the US. The stablecoin market today is comparatively tiny at ~$230b, 99% of which are stablecoins pegged to the US dollar.

As Stripe notes, stablecoins have “four important properties relative to the status quo”:

“They make money movement cheaper, they make money movement faster, they are decentralized and open-access (and thus globally available from day one), and they are programmable.”

These properties may allow stablecoins to reach further than the Eurodollar market does currently. Eurodollars today are mostly in European financial centers (ex: UK, Switzerland) and are dominated by corporate use cases. The people who need dollars the most (individuals in countries with high inflation or economic mismanagement) aren’t really served by the current Eurodollar market. If you are an individual in Brazil, getting a USD bank account or USD loan is still extremely difficult.2

Of course, stablecoins don’t have the same protections that bank deposits in the US have, like FDIC insurance. But neither do Eurodollars! If a foreign bank goes under and has your USD bank account, the Fed and Treasury are not bailing them out.

That’s why Austin Campbell, professor at NYU's Stern School of Business and the CEO of stablecoin company WSPN USA, predicts “over the next … 20-ish years, probably the entire Eurodollar market is moving to stablecoins.”

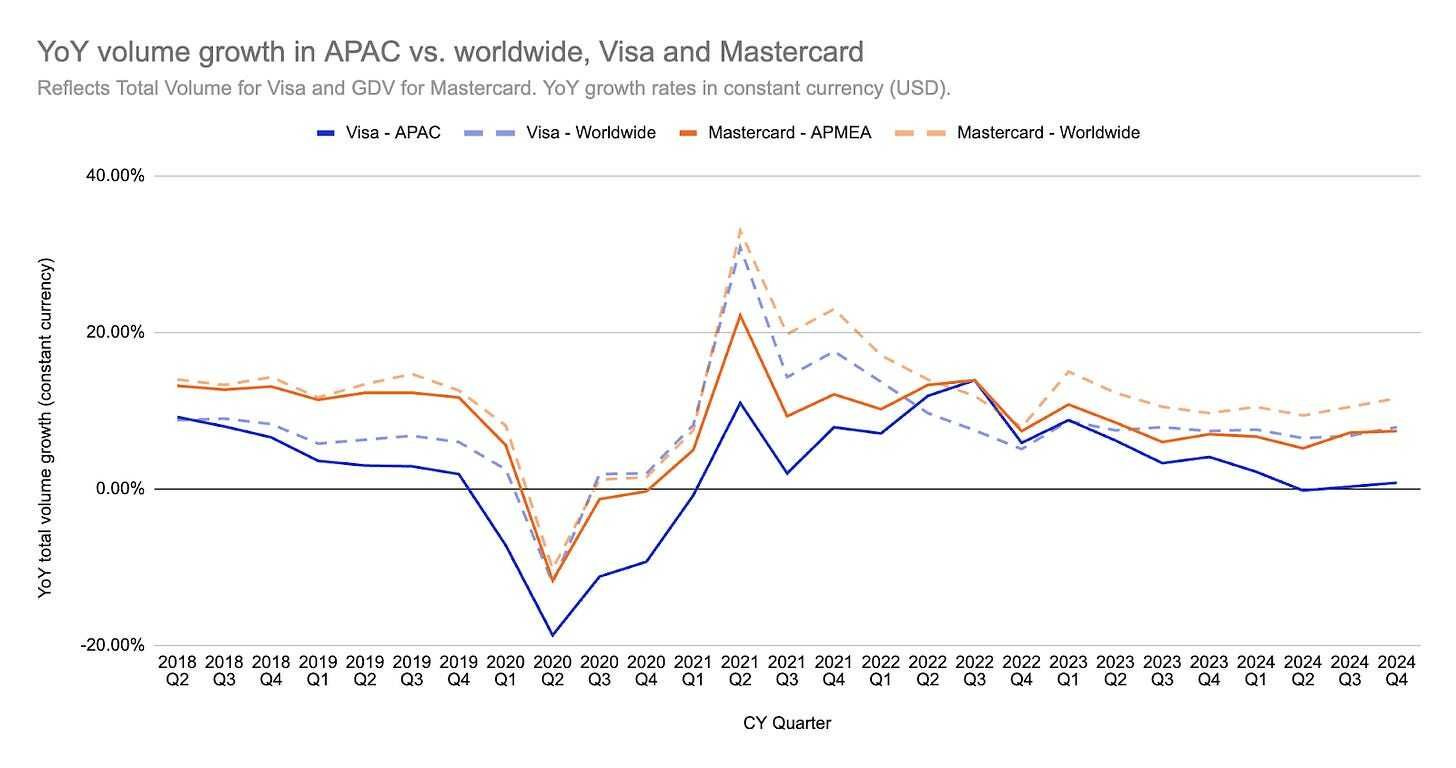

Cracks in Visa’s business?

Source: Publicly available earnings reports

This chart focuses on quarterly growth rates for Visa and Mastercard, with special attention on APAC (Asia‐Pacific). These networks have long been viewed as unstoppable growth machines—both typically report steady double‐digit volume increases year after year. And while this is still happening at the worldwide level, Visa started to see a meaningful dip in APAC in 2H24 to ~0% growth.

They blamed a macro slowdown in China, noting growth in Asia ex-China has been fine. This seems plausible, but the more interesting question we discussed is whether this reflects China being ahead of the curve on new payment methods that will replace the card networks (Alipay, WeChat pay). If so, it would be a warning sign on the ability of the card networks to continue to grow at high rates indefinitely.

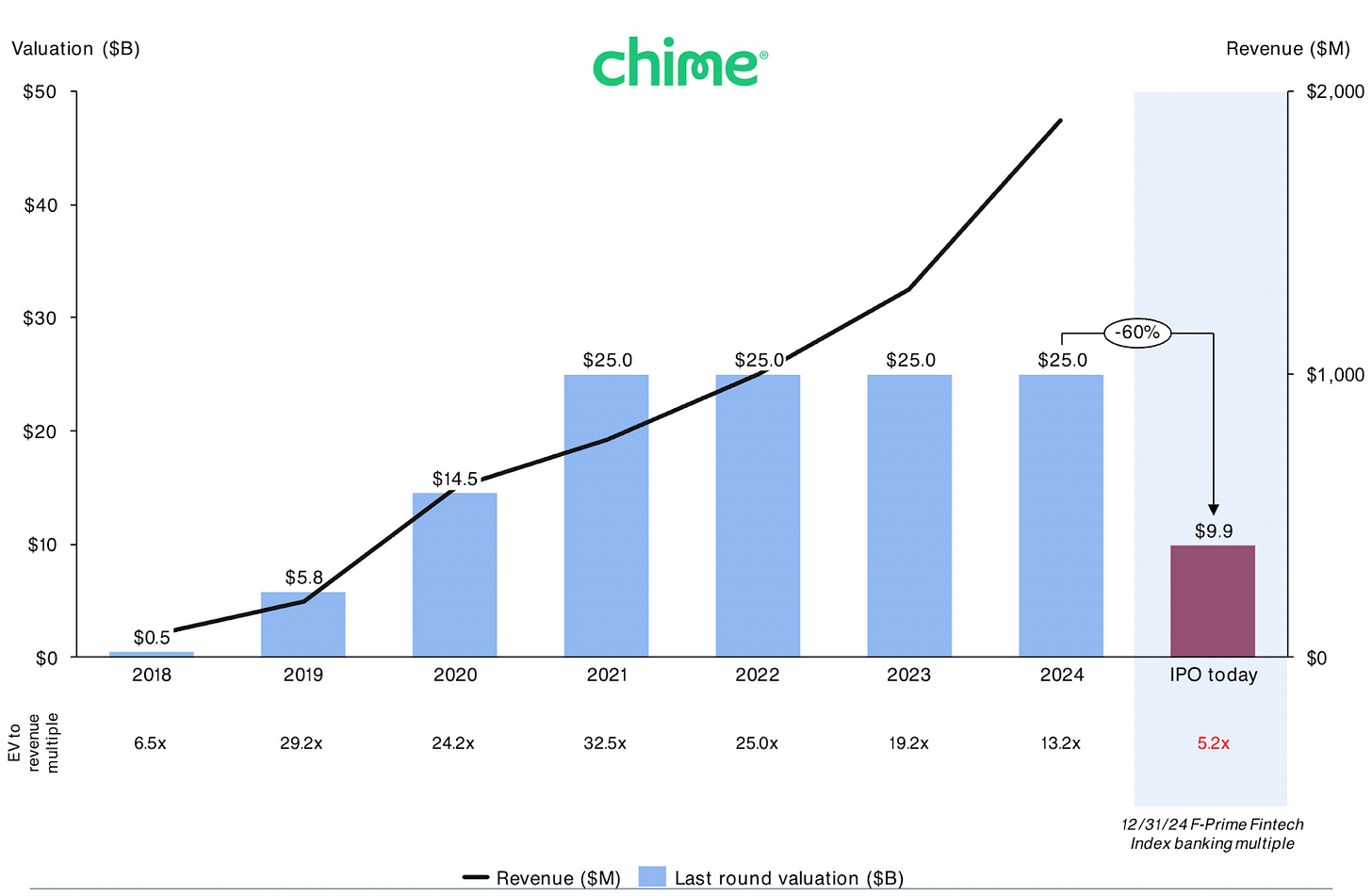

Will fintech ever trade like “tech” again?

Source

One measure of whether fintech is really “back” is what multiple fintech companies trade at. For example, Chime is expected to go public in the coming months. They were last valued at $25b in 2021 at a 30x revenue multiple and have more than doubled revenue since. But current market multiples (~5x) would make them only worth ~$10b.

At the same time, Ramp recently raised at ~20x revenue multiple, and Stripe is raising at a similar one. They fundamentally have similar business models to Chime today (fees on interchange), but both also have grand long-term visions and Ramp is growing significantly faster than Chime (albeit at a lower base). So there still seems to be room for some fintech companies to earn “tech” like multiples with the right pitch, at least in private markets right now.

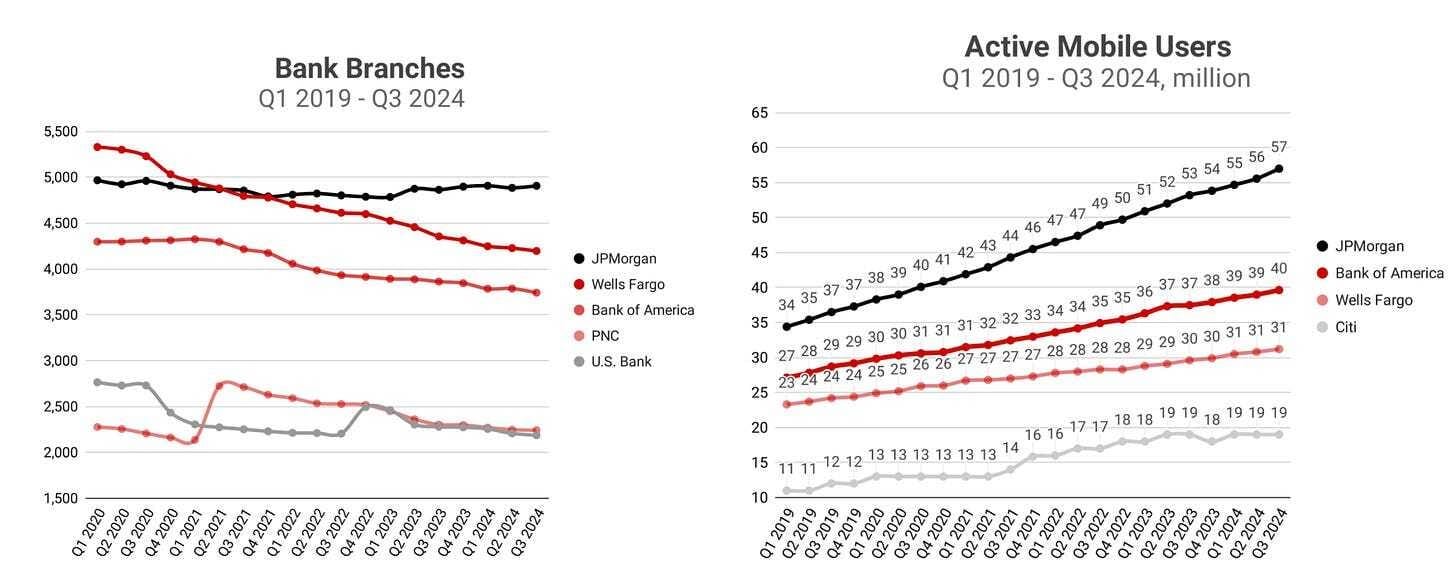

Banks are growing while shrinking their branch footprint

Source

We’ve seen a massive consolidation in commercial banks in the last 3 decades, going from ~14,500 in 1985 to ~4000 today. Among the largest banks still around, we’ve seen a decline in bank branches since COVID (except for JP Morgan) and a huge rise in active mobile users (and deposits).

A big discussion theme was whether large banks are better able to take on fintechs having improved their technology capabilities in recent years. Having a mobile app used to be a pretty effective wedge in fintech 10 years ago (Robinhood was mobile-only to start!) but now it’s table stakes and most banks’ apps/websites are pretty good. Fintech companies may still be better at customer acquisition but there is a general sense that banks are catching up. As one person put it, “Banks are not stupid, just slow.”

Many fintech banks don’t have physical locations (ex: Sofi), so it makes you wonder why banks still have as many branches as they do. One reason is….

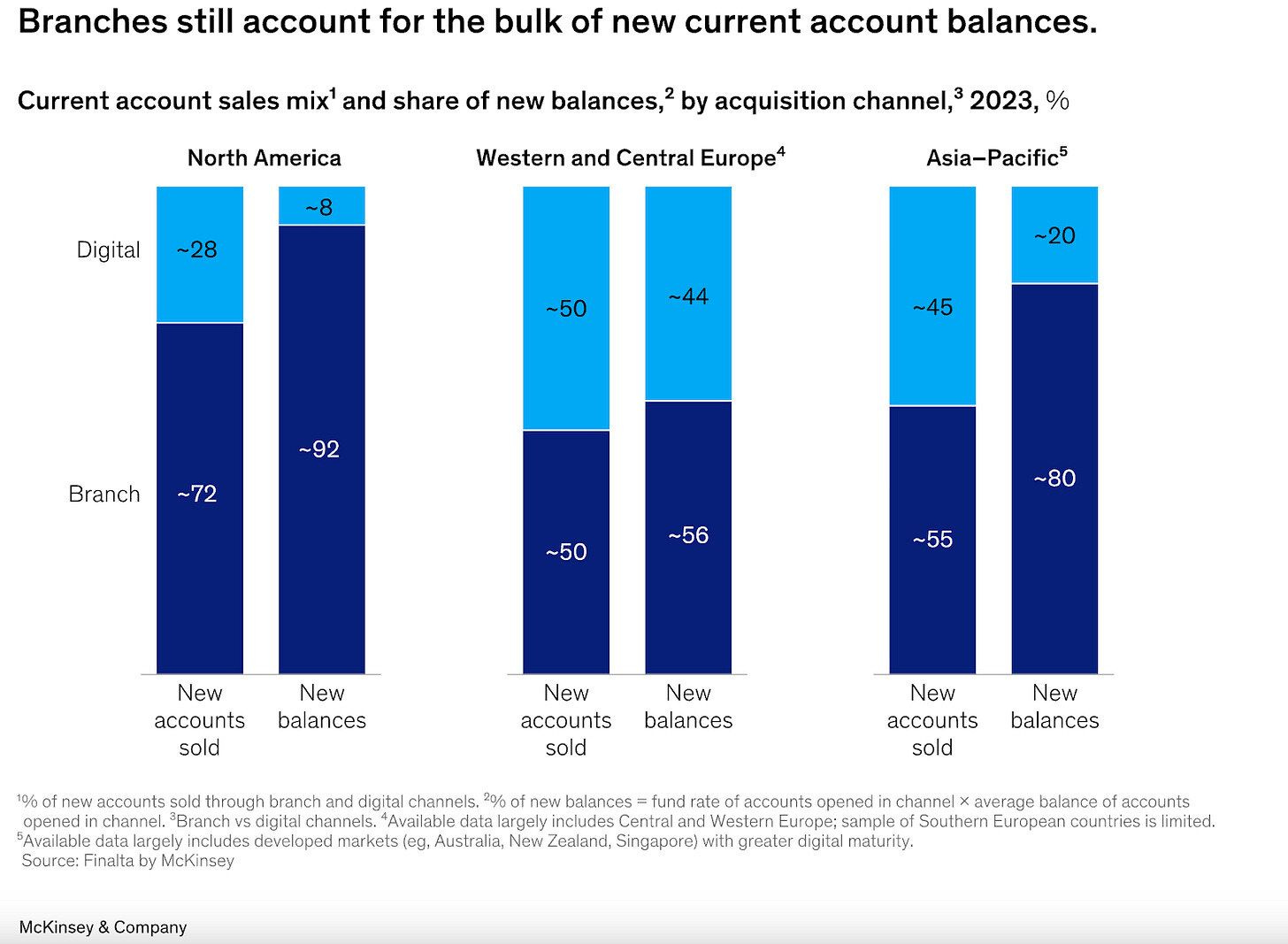

Bank branches still account for the bulk of new account balances

Source

… a shocking amount of new deposits still come from branches! In North America, 72% of new accounts are sold through branch channels, bringing in 92% of all new dollars. I was personally surprised by this. I understand some things are better to go into a bank branch, but it feels like you can do almost anything digitally today. In-person trust still matters, and I’m an out-of-touch coastal millennial I suppose.

It’s why companies like Capital One are building up their in-person presence with Capital One Cafes (other banks are following).

1 Outside of digital gold (Bitcoin) and speculation/gambling

2 Some of this is due to regulation, as governments want to prevent the selling of their local currency for dollars. I’m sure these governments will eventually attempt to regulate stablecoins similarly but it will be more difficult given they can’t regulate intermediaries as easily (like they do banks today) and a lot of the population is already using them.