I’m betting on sports exchanges

If you’re reading this and haven’t joined Interspace, join now to get new posts as they are released. If you’re already an Interspacer, invite a friend you respect to join.

If you know me, you know I’m a huge Duke fan. My first year was when Jon Scheyer captained the national championship-winning squad in 2010. So March Madness is a big deal for me. I watch as many matchups as I can while filling out a bracket usually ruined by the end of the round of 64 (which needs a better name like “Big 64” or “Nintendo 64”).

When Robinhood announced they would work with Kalshi and DerivativesX to surface March Madness prediction markets in-app, I couldn’t believe my fintech and sports worlds were colliding and I had to check it out.

I’ve always been interested in sports betting as a non-correlated supplement to stock market investing, but I found the practice arcane and uninviting, often requiring sophisticated knowledge of unintuitive terms and access to questionable gambling websites that only accept cryptocurrency. Robinhood’s promise to democratize access and simplify the market like they did for stocks, options, and crypto resonated with me, and I knew that, more than beating the odds, it would be a good way to learn how fintechs could innovate on and improve a legacy practice.

Some people think Robinhood shouldn’t enter sports betting, but they are making broad generalizations and big assumptions that hinder their ability to think through their reservations. First, we should define what we’re arguing about and ensure the legal foundations are clear.

When we talk about betting on sports, there are two major ways to do this:

Sportsbook-based sports betting (“traditional” sports betting): A centralized entity (the bookmaker) determines the odds for a sports event and provides pricing (the spread) for the outcomes, inclusive of their fee. Bettors place bets against the bookmaker, who balances the spread between bettors on both sides to pay winners.

Sportsbooks’ business model relies on determining the spread and optimizing based on real event odds, as it dictates the bookmaker’s revenue (e.g. DraftKings, FanDuel).

Since the bookmaker sets the odds and payouts, there’s no federal regulatory body governing these entities. This leaves legality and enforcement to the states.

Exchange-based sports betting (“new age” sports betting or “sports trading” or “sports prediction markets”): An exchange provides a platform where bettors can bet directly against each other, rather than against a centralized bookmaker. Sports event contracts are largely binary (win/lose) rather than based on point differentials, initial odds are set at 1:1, and the market determines the spread through buying and selling event contracts with a small per contract trading fee. After the event, the winners take money from the losers.

The exchange-based sports betting model depends heavily on platform trading activity. The exchange doesn’t care who wins or loses, only that many people are trading (e.g. Kalshi, DerivativesX, Robinhood).

Since the exchange is a platform for facilitating trades, federal regulatory bodies like the CFTC govern these entities and provide legality and enforcement at a federal level.

In short, exchange-based sports betting:

operates on a federally regulated, open platform where odds are clear via the market order book.

allows trading against other bettors instead of a centralized bookmaker, reducing incentives to lower bettor odds.

allows live, real-time unlocked bets that can be closed out or added to at any time during an event

Now, in order to engage in this debate, we need to understand Robinhood’s position and the regulations. Sportsbook-based sports betting is federally allowed and legal in 40+ states, and the practice will continue regardless of Robinhood’s participation. Traditional sportsbook-based sports betting is associated with negative perceptions of gambling including dark patterns that encourage high-risk plays like parlays, adversarial odds-setting, and access cutoffs for players that “beat the house.” This type of sports betting can have negative expected value when spreads are determined in a black box way and bettors on both sides interact with a bookmaker, not each other.

But despite being legal in many states, Robinhood isn’t even operating in the sportsbook-based sports betting space. Robinhood, Kalshi, and DerivativesX are in the exchange-based sports betting space. In this space, bettors trade directly against each other, and the expected value is zero, not negative (other than the nominal fees). The fees are transparent, and it’s in a platform’s interest to make the spreads as clear and real-time as possible to encourage trading. Robinhood is actually one step removed in that it surfaces the contracts that Kalshi/DerivativesX provide in a user-accessible way. Stopping Robinhood from accessing exchange-based sports betting only stops good UI, not the practice itself.

There are at least five arguments against sports betting:

1. You think sports betting should be illegal and fintechs shouldn’t be able to enable it

If you have an issue with fintechs engaging in sports betting, talk to your legislator to change the legislation. Don’t stop companies from operating legally. You should also justify why we legalize vices like cannabis, alcohol, and smoking but want to crack down on gambling. Explain why banning sports betting will lead to better outcomes than Prohibition or other attempts to ban vice versus drive incentive alignment via penalties.

I don’t like profiting off vice, but let’s not apply rules to one versus another or claim to know what’s best for Americans. Evidence shows sports betting can engage consumers and have an economic impact (over $300bn annually). Despite the charged topic, 80% of US states have legalized it. The people voted for this - why should you determine its enablement?

2. You think sports betting should remain as it is because it’s efficient and well regulated

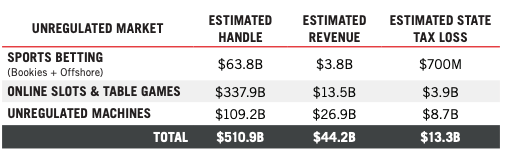

Are we discussing the same industry where two major players face hundreds of class action lawsuits and have settled for millions? You’re defending an industry where centralized sportsbooks operate an oligopoly with FanDuel and DraftKings controlling 70% of the legal market and the top four players comprise 90% as somehow “good” for society? Or are you satisfied with the fact that despite progress on online betting, 60% of all sports betting occurs on unlicensed platforms with no consumer protections and high exploitation risk? I hope that’s not the position you chose to defend.

3. You think that sports betting is more dangerous and less “good for society”

This is patronizing and inconsistent. How are trading memecoins, 3x leveraged tech shares, zero day options, bitcoin ETFs, and index options “better for society” than sports betting? If you believe this, I have some SPACs, penny stocks, and dividend arbs to sell you.

Some may argue that holding stock is more long-term than sports betting. I would point them to the rise in day-trading, memecoin investing, and the declining average hold duration. Why hold onto a stock when we have real-time information on its trend and finfluencers claiming to know our investment moves? I would also ask you to justify why people invest in financial engineering and price improvement like the market-makers driving 80%+ of market volumes.

4. You think banks and fintechs should only provide services for financial health

Have you ever shopped for financial services in America? Alongside Robinhood’s prediction markets are high APR cash advances, payday loans, memecoins, hyperyield-bearing stablecoins, high fee earned wage access products, shady alternatives, complex real estate investments, and stock market derivatives, all available at a bank or brokerage. Robinhood should not be the only one above your line while Schwab, Fidelity, and E*Trade are saved from ire. And maybe go after those big banks that provide for financial wellness but have caused $20B in overdraft fees, predatory lending, and reductions in financial access.

5. You think sports betting is too risky, so we should ban it outright or prevent fintechs from having access

I find it hard to believe that sports betting is riskier than other investments allowed for regular investors and enabled by fintechs. Real estate trusts, home flipping, crypto, venture investments, hedge funds, infrastructure funds, etc. Why do we draw the line at sports betting when many are riskier, especially on an exchange with binary outcomes, making the chances 50/50 for most bets?

If we have issues with regular retail investors adding “sports betting” to their portfolio, why not use the existing investor accreditation feature instead of banning or limiting fintech access? There’s no reasonable argument to bar a savvy investor from investing in legal sports betting.

The power of prediction markets

The backlash against Robinhood stems from a misunderstanding of exchange-based vs. sportsbook-based sports betting. The claims that Robinhood isn’t “democratizing finance” or seeking truth are also incorrect. By allowing more regular investors access to the sports betting market, it democratizes finance (reducing fees and increasing transparency).

But more profoundly, having bettors determine the markets ourselves is crowdsourcing and amplifying intelligence gathering, increasing our ability to pursue truth. Dismissing prediction markets’ power due to the near-term sports applications misses the point.

Instead of waiting for closed-door meetings and filtered public disclosures to understand interest rates, we can utilize the hive mind to gauge expectations in real-time. We will no longer be limited to quarterly government reports rife with errors or talking points from politically influenced leaders; we can go to prediction markets for the truth. If you can’t grasp prediction markets, look at the stock market’s real-time access to a company’s performance compared to their one-sided shareholder letters and quarterly earnings reports.

I’m excited about prediction markets, not just for March Madness sports betting (forget stale brackets for real-time betting each round) but for all national financial KPIs and international metrics.

We’re putting our money where our mouth is, and that’s a good thing.