In fintech, sometimes you need a Goliath to fight other Goliaths

The Capital One + Discover merger is happening, and that's actually a good thing

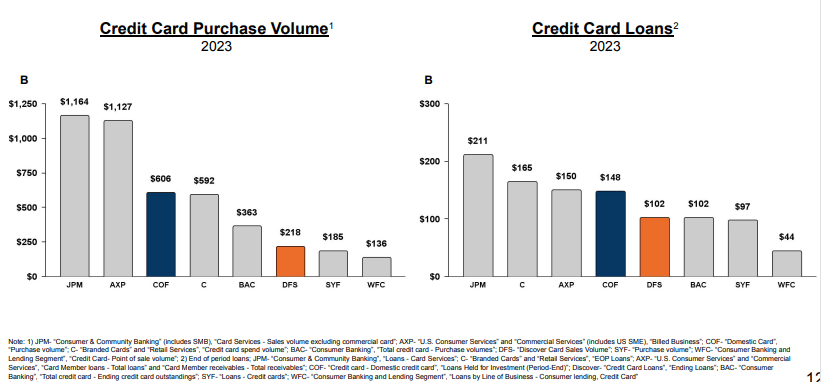

After a little more than a year, Capital One completed its $35B acquisition of Discover, combining two smaller players into a larger force. Discover brought its payments network of 70M merchants, Pulse debit network, and ~300M debit & credit cardholders with ~$84B of consumer deposits. Capital One had 25M+ credit cardholders, $350B of deposits, and a large network of fee-free ATMs.

When the announcement of the transaction occurred, politicians, pundits and regulators claimed it would be detrimental for consumers because:

It created another giant bank that would eliminate banking competition.

It would limit consumer access and services.

It would exacerbate the network duopoly problem.

These arguments are not accurate. Now that the transaction is completed and implementation is starting, it’s time to revisit and break them down.

Myth #1: Capital One + Discover create a giant bank that eliminates competition.

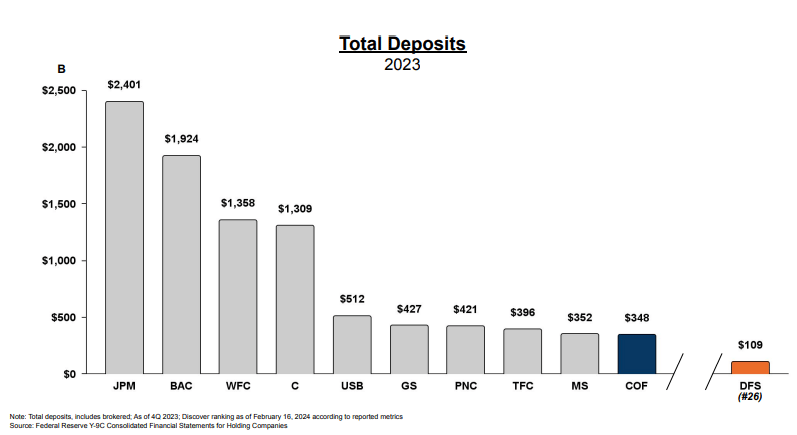

Let's address the elephant in the room: the "too big to fail" argument. Critics cite the combined assets of Capital One and Discover as making the 6th largest bank in the U.S., proving regional banks will be crushed by this acquisition.

The argument relies on a flawed interpretation of perfect competition in banking. In this interpretation, the best economic outcomes result from many banks with no single one influencing the market price of banking or access to services.

But this view needs context. We don’t operate in a world of perfect competition for banking services but one dominated by systemically large banking institutions that can’t fail. Sure, Capital One becomes one of the largest banks compared to regional institutions, but what about the “little old” JPMorgan Chase, Citi, and Wells Fargo that CO-DF will also be fighting? Even combined, CO-DF will have 70% fewer deposits than the smallest of the Big 4 systematically important financial institutions.

The "too big" narrative ignores a key reality of modern banking: scale is necessary to deliver competitive services. Without sufficient scale, banks can't afford to provide scaled banking services, leading to worse service, limited underwriting, and higher customer costs. Larger banks have ~35% better loan economics, 30% lower expenses, and are better regulated than smaller ones.

posts.interspace.ventures/p/overbanked

We're not creating a new megabank. Instead, we're enabling an existing large bank to better compete with larger incumbents. That's how you drive real innovation in financial services. Sometimes you need a Goliath to fight other Goliaths.

Myth #2: The Capital One + Discover merger limits consumer access and services

Critics of the merger are so focused on the "big bank" narrative that they are missing how the customer bases and product offerings complement each other. This merger is about addressing gaps in each company's portfolio.

Capital One has mastered premium credit cards and tech-forward banking but struggled to expand their debit and everyday banking presence. Meanwhile, Discover has built a loyal following with cash-back rewards and US-based customer service but never cracked the premium card market.

This combination enables a unique full-service financial platform that can compete across all segments while maintaining the customer service that made both brands successful. Capital One's efficient self-serve technology and Discover's renowned US-based customer support create a service model that JPMorgan Chase and Wells Fargo cannot match.

The technology angle is crucial. Over the last decade, Capital One spent on digital transformation to disrupt itself before fintech could. It pushed for cloud migrations, labor force transformation, and a focus on using data to self-serve, personalize, and better serve its customers.

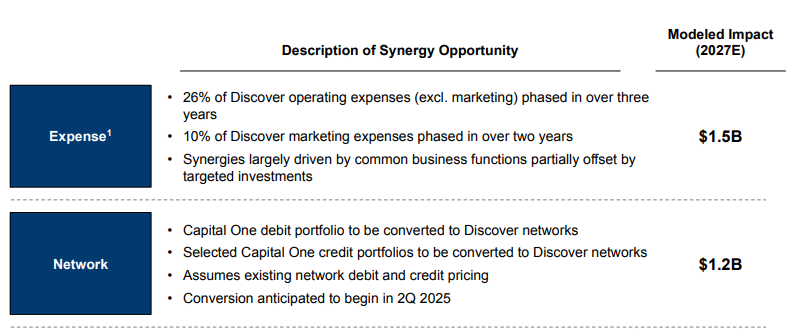

Sandeep Sood, former VP of Engineering at Capital One, says it now has the best technical infrastructure of any US financial institution of similar size - it’s “the world’s largest fintech.” Capital One is bringing that expertise to overhaul Discover’s legacy technology and infrastructure, anticipating ~$3B of annual operating and network synergies.

Critics arguing this hurts competition have it backwards. The combined entity will force other banks to improve their digital capabilities and customer service to keep up. That's how real competition works; it drives innovation and better customer experiences.

Myth #3: Capital One + Discover would worsen the network duopoly.

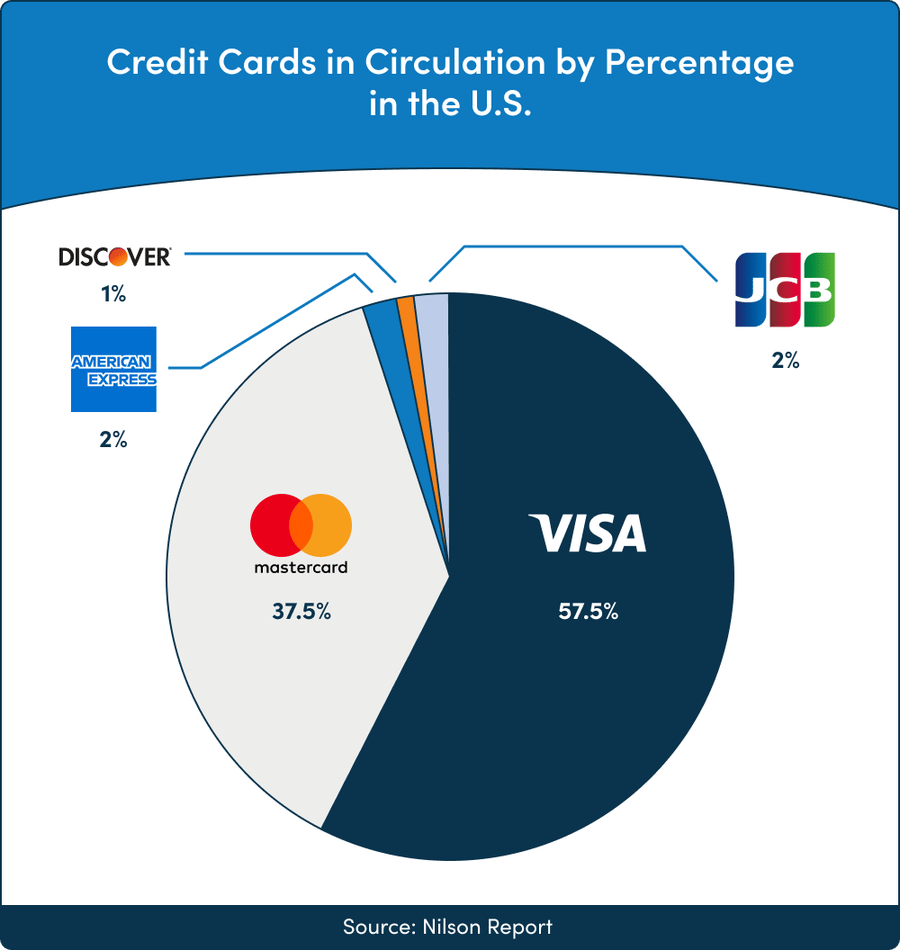

Let's start with the facts: Visa and Mastercard dominate payment networks with a combined market share of over 94% of US credit cards. The remaining players - Amex, Discover, and regional networks - fight for the leftovers. The network effects make it nearly impossible for smaller players to compete.

Think about it this way: A new payment network needs both merchants to accept it and consumers to use it. Merchants won't accept a network without consumer volume, and they won't choose a card that's not widely accepted. It's the classic cold start problem that has protected Visa and Mastercard's duopoly for decades.

This is why we so desperately need competition and a large player to compete. Small networks have failed to make meaningful inroads. A recent Fed study shows that despite 15+ minor networks in the US, they've had minimal impact on interchange rates or merchant acceptance (I'll bet only a few of you fintech nerds know Jeanie, Shazam, Maestro, NYCE, START, Culliance, Accel or the one I just made up because the brands are so unfamiliar). The painful truth is that you can't fight network effects with subscale solutions.

Capital One + Discover change this dynamic. Even combined, they will still be smaller than Visa or Mastercard, but they have the scale and resources to compete. Here's why this matters:

Capital One has massive consumer reach through its credit card base.

Discover brings an established merchant network and payment rails.

Together, they have the technology and capital to increase acceptance.

Capital One + Discover could be the first real challenge to the payment network duopoly in decades, benefiting everyone (including even Visa & Mastercard who thrive in competition but may have forgotten along the way).

The Real Opportunity: Scalable Banking-as-a-Service

While everyone's focused on traditional banking, they're missing the biggest opportunity. This merger positions Capital One to lead the Banking-as-a-Service (BaaS) space. Here's why that matters.

The BaaS market is fragmented between smaller players like Green Dot and regional banks monetizing their charters. But none have the technical capabilities and scale to serve major fintech partners effectively. Capital One + Discover changes this.

The banks that power your favorite fintechs

posts.interspace.ventures/p/the-banks-that-power-your-favorite

Consider the assets this combination brings to BaaS:

Capital One's automated underwriting capabilities

Discover's payment network and settlement infrastructure

Combined fraud detection and risk management systems

Massive data sets for better decisioning

Technology-focused approach to banking services

This lays the foundation for next-gen fintech partnerships. Imagine:

Co-branded cards with automated instant decisioning

Built-style partnerships leveraging both debit and credit rails

Embedded banking solutions with real-time fraud detection

Direct access to a competitive payment network

We've already seen hints of this strategy. Capital One has been investing heavily in API infrastructure and cloud capabilities. Discover has been quietly building its digital banking platform. Together, they could offer what every major fintech wants: a full-stack banking partner with modern technology and competitive economics.

This isn't speculation. The investor presentation highlights technology investment and partnership opportunities. They're thinking beyond traditional banking - they're building the infrastructure for the next generation of financial services.

The Big Picture

The Capital One-Discover merger isn't just about creating another big bank. It's about building the first modern financial infrastructure company at scale. This combination has the potential to:

Force traditional banks to compete and introduce competition among the Big 4 SIFIs.

Increase customer access and services while supercharging tech.

Break the payment network duopoly for good.

My fintuition tells me we'll see this deal as a turning point in financial services, not because it created another big bank, but because it created the first real challenger to decades-old industry structures.

The critics aren't wrong that this deal will create a larger bank. They're wrong about why that matters. Will Capital One + Discover reshape financial services? That depends on execution. But for the first time in decades, we have the potential for real change in payment networks, banking infrastructure, and financial technology.

Sometimes you need to build something big to break up something bigger. This deal might just do exactly that.