Bilt to Last

Bilt is back in the news, but not for a misunderstood bank partnership that everyone wrote off as unsustainable. It’s for rumors they’re attempting to raise at a whopping $10B valuation, making them unofficially a decacorn if true. While I agree the valuation is generous, I disagree with the critics that Bilt struck a bad deal. By extension, it’s clear the Bilt partnership with Wells Fargo and Mastercard is a smart and replicable one, and startups should copy it (WSJ gave you the playbook, and Bilt’s recent update to valuation shows it works).

They Bilt a Housing & Neighborhood loyalty network

To understand Bilt, we need to explain its platform and business model. At its core, Bilt is a rewards network and loyalty program. It is an enhanced and streamlined affiliate network.

Here’s how it functions:

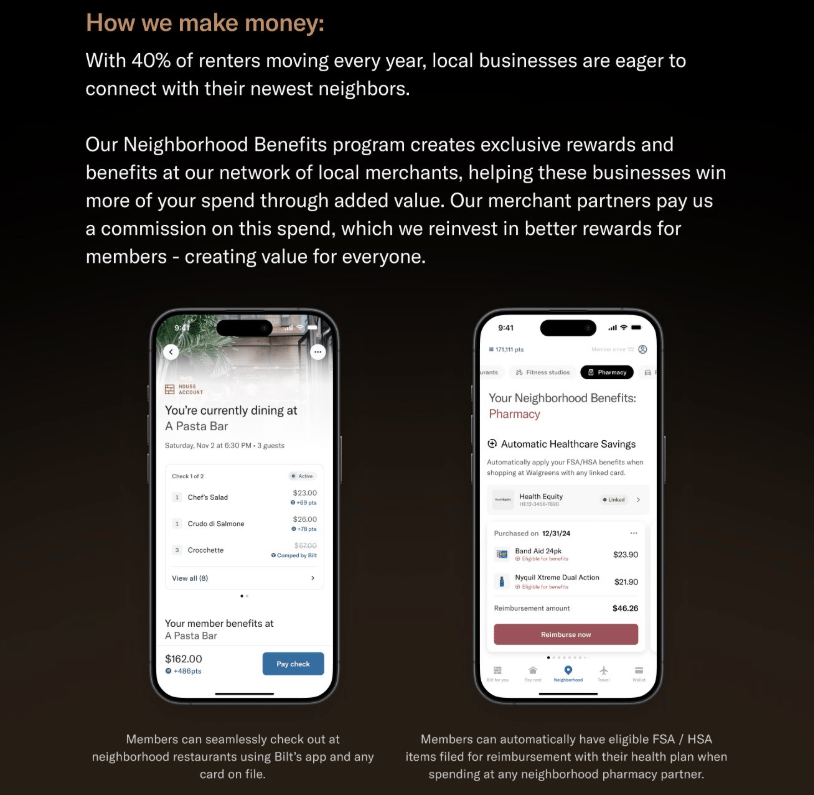

Merchants go to Bilt for access to their userbase.

Bilt works with the merchant to structure an appealing rewards offer, like significant cashback, to bring users into the store.

The merchant agrees to provide a 10% bounty. Bilt offers users 8% back in points, keeping the 2% on every transaction.

Everyone wins. Merchants attract more users at a comfortable price. Users get significant cashback and discover new merchants. Bilt makes a tidy sum at nearly 100% gross margin.

The economics can be better for Bilt and the merchant because, while the headline is perceived as 10% cashback, it’s actually 10 points per dollar and the business of points is a whole different ball game. They must be redeemed to matter and there’s a drop-off of up to 40% in points spending. The points to cashback transfer is only 1:0.5 so 1 point is worth $0.50 cashback. A merchant can offer 10% cashback and be comfortable knowing it’s only 3-5% cash out the door.

posts.interspace.ventures/p/the-business-of-free

They Bilt a viral user acquisition engine

How did they build a strong userbase to get merchants excited about marketing to them? That’s where Bilt’s value proposition came in - points on rent, for any building no matter what. Recently, the CEO, Ankur Jain, explained this:

At its core, we started Bilt to reward people on their biggest monthly expense, which is rent. And it’s funny because it’s one of those things where people have totally taken it for granted. But you spend 30%, 40%, in some cities 50% of your income on housing costs every single month, and, yet it’s the one category that hadn’t really been modernized to the way that the rest of the payments ecosystem has evolved. I mean, if you’re under 35, the only reason you probably have a checkbook still is for rent. So can you digitize that, and can you do what other payment worlds have done, and bring rewards into the experience?

First, let’s set the economics aside for a moment to understand mechanically how rental payments via Bilt work. There are two ways Bilt makes that happen:

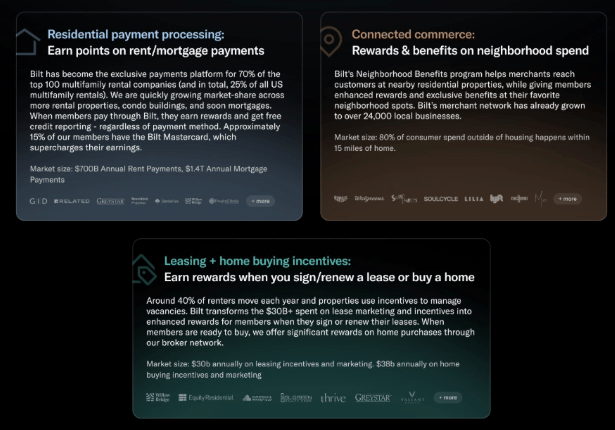

Direct property integration: Bilt integrates directly with the rental property. This enables seamless, instant, on-time payments for landlords while providing a feature renters want. Bilt monetizes payment processing like a standard processor.

Indirect property integration: Bilt offers a smart workaround for properties that haven’t integrated with Bilt. They set up a shadow bank account for users where the company provides just-in-time funding for rent payments off their own balance sheet and debits your credit card. While it doesn’t generate economics on its own, it expands their reach and increases user acquisition while avoiding the credit card processing fees landlords charge.

Together, Bilt can credibly market a claim of providing points on rent for any building that accepts bank payments.

Share this post from Interspace

They Bilt valuable (& replicable) strategic partnerships

Points on rent is an amazing benefit, but so is 100% cashback. It doesn’t matter unless you can build a sustainable business model around it. That’s where Bilt’s two key strategic partnerships come in.

Mastercard

Mastercard has stayed out of the headlines, but it is a key part of the strategic partnership ecosystem Bilt created. Normally, rent payments over the network incur substantial network fees that make them unsustainable (hence the high credit card processing fees or inability to use your credit card to pay a landlord).

But Bilt struck a favorable deal with Mastercard to reduce or waive typical network fees. This was likely in exchange for a treasure trove of data about renters’ financial behavior that networks normally don’t see with ACH/wire transactions. Payment networks talk about “new flows” to stay ahead of any payment flows that might reduce dependence on them, like real-time payments (RTP), FedNow instant payments, A2A transfers, or BNPL. You can bet that Mastercard values this data and would pay for it.

Wells Fargo

Restating my 2024 over-engineered year in review, the Wells Fargo partnership is the most well-known and controversial from the Bilt saga. The drama started in June 2024, the WSJ reported that Wells Fargo was losing millions monthly on its partnership with Bilt Rewards, and it turned our ecosystem upside down. The gist of the argument was the following (as summarized by Sheel Mohnot on X):

Wells Fargo assumed the Bilt card would be the top one for renters with balances, but most users use it only for rent and five required transactions.

Wells Fargo assumed 65% of card purchase volumes would be non-rent, generating interchange revenue. However, the reality was over 65% rent-related, earning very little (<40bps gross and effectively negative with cashback).

Wells Fargo assumed 50-75% of balances would be revolving and earn interest, but most don’t carry a balance and only 15-25% is revolving.

Wells Fargo is paying ~0.80% to Bilt on rent payments and hoped to cross-sell its mortgages, but that hasn’t happened yet.

The early WSJ takes that the cash back on rent payments model doesn’t work are wrong. Both WF and Bilt denied issues in the contract, which extends until 2029. It is also funny that a WSJ reporter talked to only Wells Fargo about the contract negotiation and took their word on opinions that could just be negotiation talking points. Didn’t they wonder why WF was eager to “leak” this?

Here are a few counterpoints to the article’s main points:

We’re 2 years into a 7-year partnership. It’s too early to measure top-of-wallet success. Any increase in spending is a success, and they have the actual rent payment on the card (if rent isn’t your biggest monthly spend, I want to be you).

Wells Fargo could not have thought this fact was true and the statement was misinterpreted. They said 65% of non-rent card purchase volumes wouldn’t relate to rent-related payments (e.g. utilities, maintenance, internet) and it was misstated. Wells Fargo knew the majority of card spend would be rent-related as that’s the case for every individual anyway (~50%+ spent on rent/housing). People were eager to criticize Bilt and assume Wells Fargo was foolish, but remember “Banks are slow, not stupid.”

I can’t believe this was true and this is another misinterpretation. The actual statement was 50-75% of non-rent payments would revolve. For the credit score that Bilt targeted, the revolving balance is only 20-30% or less. Getting to 50-75% would mean they’re targeting subprime creditors which aren’t eligible for the card (<580) OR they assume the core demo can revolve on rent payments (which isn’t possible or this product wouldn’t exist).

We’re two years into a 7-year relationship. At the time of the article, Bilt didn’t have an upsell motion for homebuyers. Within months, they launched a program to earn Bilt points on home purchases and revamped tools to help renters estimate monthly payments including taxes and insurance. This is just the beginning, and any smart fintech nerd can see many ways to expand the upsell opportunities.

The article hinged on a supposed $10M/month loss, but for a bank making $20B/quarter, this is a rounding error. Bilt may not succeed, but judging them by this article is the wrong way to evaluate them.

Remember Jamie Dimon’s quote on the Chase Sapphire Reserve Card’s success:

One of the fictions here is that the marketing cost ... gets booked over 12 months. The benefit of the card gets booked over 7 years. The card was so successful it cost us $200 million, but we expect that to have a good return on it. I wish it was a $400 million loss.

The article increased interest in consumer credit in the mortgage space. We saw mortgage servicing platform Haven launch in September 2024, Mesa launch in November 2024, and Further to help aspiring homeowners. This model works, it’s replicable, and startups are already doing it.

They built a self-sustaining virtuous cycle.

With these three pieces, they have what every startup wants - sustainable product market fit with a self-reinforcing virtuous cycle:

More users join Bilt for unique rental/mortgage benefits and a network of merchant rewards.

More merchants join the platform and offer more rewards due to the growing user base.

Bilt can negotiate better strategic and financial partnerships to strengthen the business model and unit economics.

When this works, it benefits all stakeholders and mints a sustainable, competitive business model. The market will reward you handsomely (perhaps too handsomely) for building in this space, as seen by Bilt’s jaw-dropping 50x revenue multiple implied by their latest rumored round, and you can do this profitably as suggested by the rumors of Bilt having been profitable since their prior round.

All that said, this valuation is still overpriced. Bilt is a loyalty rewards network, and we have many. It makes no money on the credit card (as was always their plan), so why are we valuing it like the next big neobank? They have an amazing business that should get a ~15x revenue multiple at most, taking them to $3B (which was their last round). If someone offers 2% back on rent + 1% back on mortgage and uses a company like Percents for merchant-funded rewards, I don't see how Bilt competes except on rewards pricing in a downward trend.

I credit the Bilt team for building (bilting?) a network effect and competitive moat that is hard to dethrone. But let’s remember that this network effect makes Bilt’s business model hard to replicate, not special partnerships. Startups in this space have a shot at expanding this concept and building on or adjacent to Bilt. There’s room for many winners because your competitor isn’t Bilt, but the 99% of people not optimizing their rent and mortgage spend. I’m excited to see what more fintech nerds build and how users continue to benefit from this innovation.