The Over-Engineered Guide to Building Your Child's Finance Stack

It’s been a while since I’ve published something. In early September, on the same day I published my last post on the cost of compute (eerily prescient of the tokenmaxxing debacle we face now), we found out we were expecting. Life came at me fast after that.

By October, Chime’s long-awaited IPO became an inglorious fall. In November, we backed out of what we thought was our dream home. At the same time, my physical health deteriorated as my rare genetic syndrome was impacted by medication changes. In December, we went to Aruba for a vacation (don’t go unless it’s for a babymoon!). In January, we celebrated the new year and finally saw Drunk Shakespeare. By February, I was unceremoniously impacted by restructuring at Block and realized later it was the best possible thing that could happen to me. In March, my health condition finally improved after finding a gamechanging medication. In April, I decided to start my own business and we started to see what became Knicks in five. In early May, we bought a home that’s actually our dream home.

And nine months after that last post on May 16th, we welcomed our baby girl into the world, the greatest day of my life and a life-changing moment in time.

Needless to say, the newsletter had to take a pause.To those who stuck around, thank you. The newsletter has always been a source of creativity and pride, and I’m feeling the pull of writing once again. I’m excited to make it a core part of my business going forward. You can expect more takes, more discussions and more over-engineered deep dives on a more frequent basis at least 1-2x / week (between managing diaper dilemmas, navigating feeding frenzies and taking plenty of photos).

As I’m navigating being a new parent, my top question has been: how do I give her the right financial foundation to set her up for success? So I did what any fintech nerd would do: I mapped out every fintech product, tax optimization and savings account for my kid’s financial head start. What I found surprised me. The ecosystem is deeper than expected, the products are better, and once again, fintech is foundational infrastructure.

So I’m thrilled to present the modern financial stack for your child. Here’s what the universal building blocks - Spending, Saving, Borrowing, Investing, and Protection - look like for your newborn. But first, the foundation.

Foundation: SSN, Birth Certificate, Passport

The timeline: When you file the birth certificate, the SSN process kicks off automatically - the card usually arrives in 2-4 weeks. You need that SSN to open everything below, so nothing else happens until it shows up.

Once you have it, you can apply for a passport. Infant passport paperwork is genuinely annoying (both parents present, notarized forms), so I used HelloGov to streamline the filing. Optional, but worth it if international travel is on the horizon (we’re hoping to go to London at 3 months and I’m taking recs!).

Spending: Teaching Financial Responsibility

Spending is money flowing out - and early choices teach restraint, agency, and consequences. Giving a kid their own account, even just $20/week in allowance, teaches them that money is limited, spending has consequences, and saving is a choice.

The players:

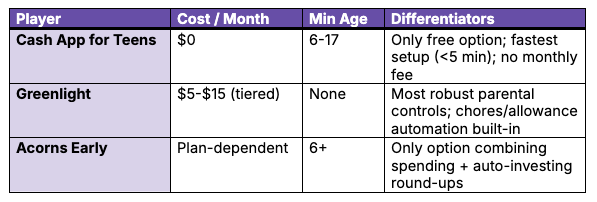

Cash App for Teens (ages 6-17): individual account ownership, parental spend controls, a debit card. Setup is under 5 minutes - the easiest onboarding I found.

Greenlight (paid, no minimum age): best for younger kids thanks to strong parental controls and chores/allowance features.

Acorns Early (bundled with paid plans, age 6+): really an investing product, useful for an “all-in-one” feel rather than spending controls.

No tax implications here. Paid “kids debit” apps add convenience, but fees compound so you’re mainly prioritizing clean UX and controls.

Saving: Dependent Care FSA

A Dependent Care FSA is a pre-tax account for eligible care expenses (daycare, preschool, after-school, approved babysitting). Pre-tax contributions mean real savings: contribute $5,000 in a 24% bracket and you save $1,200. That’s major savings to put towards childcare.

The players:

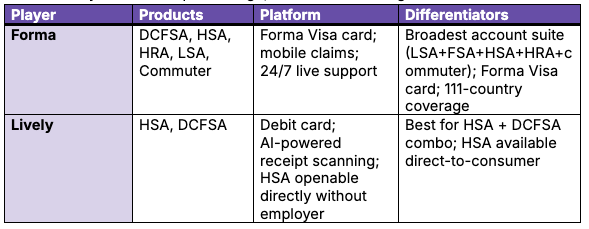

Forma: Modern, employer-first benefits platform with Dependent Care FSA support, debit card, mobile claims, and configurable grace/carryover (plan-dependent).

Lively: HSA-first administrator that also runs Dependent Care FSAs; clean participant app, fast reimbursements, and solid support (availability depends on employer).

Limits: up to $5,000 per household (MFJ, single, or HOH); $2,500 if married filing separately. Watch the use-it-or-lose-it rule - some plans offer a grace period or limited carryover. The cap isn’t huge, but it beats nothing.

Borrowing: Building Credit Early

Borrowing capacity is the ability to access credit in the future. For kids, you can lay groundwork by adding them as authorized users (AUs) on your card so long as the issuer and bureaus report those tradelines. Strong, long, clean credit history unlocks better rates later. Start early, keep utilization low, never miss a payment.

The players:

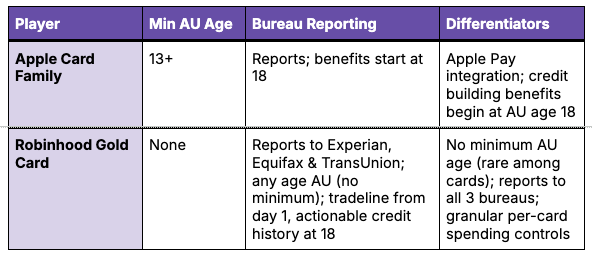

Apple Card Family: Add participants 13+ with spend controls. Reporting benefits generally start at 18.

Robinhood Gold Card: Add children as AUs with no stated minimum age and granular controls. Layla is already an AU on our card today

Two things matter most: reporting (verify the tradeline posts for your child’s age and to which bureaus) and discipline (keep utilization under ~10%, pay on time every time - your behavior shapes their file).

Investing: Creating Lasting Wealth

For a newborn, investing is measured in decades of compounding.

A $10K investment at age 0, growing 7% annually, becomes ~$430K by age 60. The same $10K invested at 18 becomes ~$150K. Time is the whole game - and your newborn has 18 years before they can legally touch it. There’s now four primary vehicles:

A) 529 Plans - Education-Specific

After-tax contributions, tax-free growth if used for qualified education expenses (tuition, room & board, books, supplies, some computers). Contribute $20K by age 5, watch it grow to $50K by college without any additional dollars in, and those gains are never taxed. Some states add a deduction or credit - check yours.

The players:

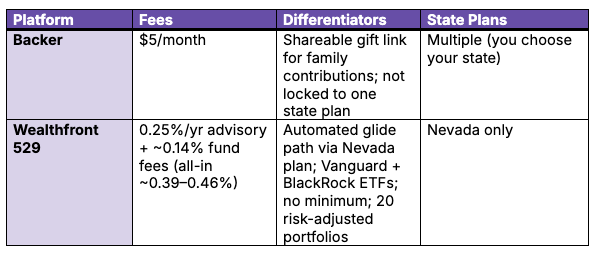

Backer: A modern 529 platform with investment management and family gift coordination. I’m using Backer today and I love the experience.

Wealthfront 529: Automated 529 via Nevada’s plan with algorithmic glide path; shifts from aggressive to conservative as college approaches; 0.25% advisory fee + ~0.14% fund fees; no minimum.

Remember that annual gift exclusion is $18,000 per donor ($36,000 gift-splitting); you can front-load 5 years at once (~$90K per donor). Aggregate caps vary by state, often ~$300K-$550K+. The tradeoff is the education-only restriction - non-qualified withdrawals trigger taxes plus a 10% penalty on gains. Recent rules allow limited 529-to-Roth IRA rollovers under specific conditions.

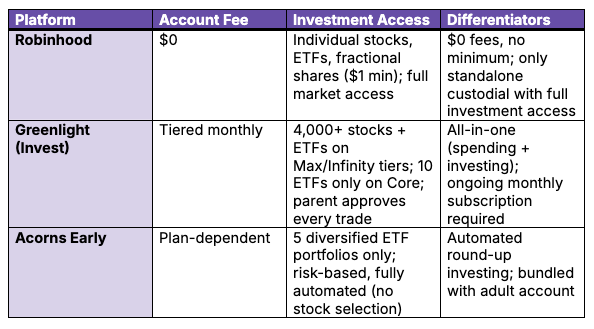

B) Custodial Brokerage (UTMA/UGMA) - Flexible

Brokerage accounts in your child’s name that you manage until transfer age (usually 18-21), then they get full control. No contribution limits (subject to gift tax rules), broad investment access, withdrawals anytime for the child’s benefit. The “kiddie tax” may apply to unearned income above a threshold.

The players:

Robinhood: $0 fees, fractional shares, clean UX, ~10 min setup. Best if you’re budget-conscious and want it alongside your own investing. I use this now and have found it to be a seamless experience.

Acorns Early: Offers custodial investing as part of a paid plan. It has occasional promotions, so evaluate total subscription cost versus assets. It is costly for low-value accounts.

Greenlight: Also offers custodial investing on paid tiers. All-in-one convenience, ongoing cost: one app for chores, card, and investing, but you’re paying a monthly subscription and accepting a curated investment menu.

Remember that custodial accounts become the child’s asset at transfer age, so set guardrails and expectations now.

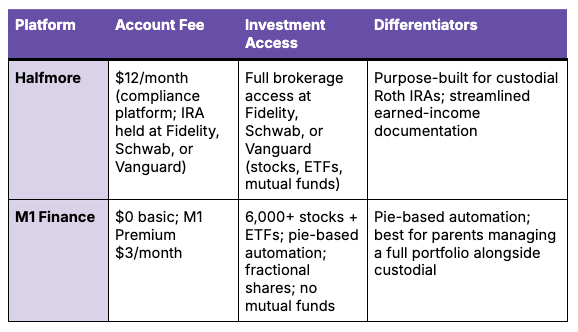

C) Custodial Roth IRA - Early Retirement

The most powerful long-term vehicle if you can meet the earned-income requirement. Contributions must equal documented earned income; growth is tax-free. $10K contributed at age 10 at 7% becomes ~$430K by 60 - all tax-free.

The players:

Halfmore: Modern UX, fractional shares, low-fee workflow. Check that custodial Roth IRA is available and confirm earned-income documentation requirements.

M1 Finance: Pie-based investing, automation, fractional shares. Check custodial Roth IRA availability for your account tier before opening.

Remember that the earned income must be legitimate and defensible to the IRS (modeling, acting, freelance, a real family-business role). 2025 cap is earned income or $7,000, whichever is less. If you’re trying to move $7K out of your business without justification, the IRS will scrutinize. Roth contributions can be withdrawn penalty-free; earnings are locked until 59 1/2 with limited exceptions.

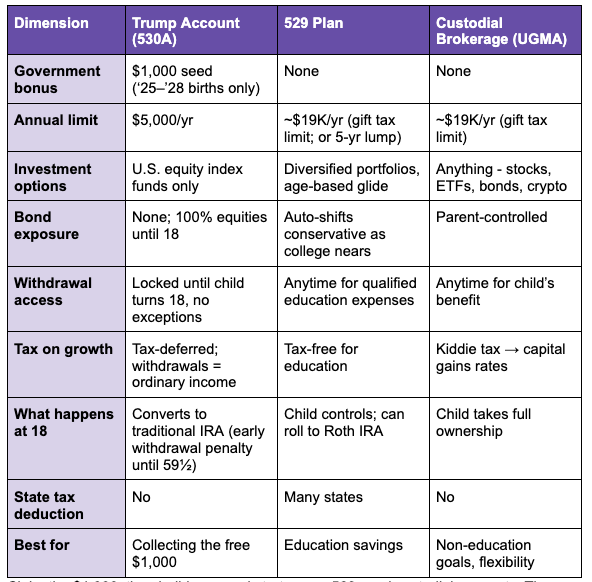

D) Trump Accounts (530A Plan) - Take money and run

Trump Accounts are a new type of IRA introduced through the OBBB and designed to encourage retirement saving for children. If your child was born between 2025 and 2028, there’s a $1,000 federal seed deposit waiting for you. And the Dell Foundation is giving away an additional $250 for the first 25M kids who sign up.

Here’s the reality: Trump Accounts are structurally inferior to both 529 plans and custodial brokerages on nearly every investing dimension. They’re capped at $5,000/year, limited to U.S. equity index funds only (no bonds, no international exposure, no diversification as college approaches), and completely locked until your child turns 18 with zero exceptions, no emergency access, nothing. At 18, the account converts to a traditional IRA, meaning all growth is taxed as ordinary income when withdrawn, not at capital gains rates, and not tax-free the way a 529 is for education.

Use this as a bonus layer, not a foundation. Claim the $1,000, then build your real strategy on 529s and custodial accounts.

How to Prioritize

Fund a 529 first, at least up to your state tax benefit. Build a custodial brokerage for non-education goals. Add a custodial Roth IRA in any year income - and max it if you can. And only if you’ve done all of the above should you think about contributing to a Trump Account.

Protection: Insurance and Estate Planning

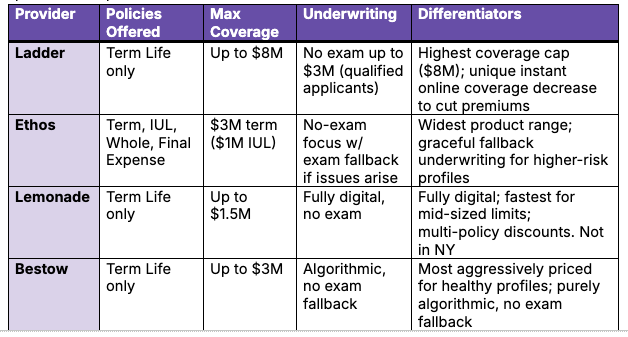

Insurance is buying certainty against catastrophic financial loss. Term life insurance covers you (the parent) against premature death, ensuring your child’s financial security. If something happens to you, who funds college, childcare, housing? Term life insurance ensures financial support.

The players:

Ladder: Term life only, coverage up to $8M. No medical exam required up to $3M for qualified applicants. Competitive pricing and standout ability to instantly decrease coverage online to lower premiums.

Ethos: Multiple offerings - Term coverage up to $3M (IUL up to $1M). Optimized for no-exam paths with automatic shift to simplified-issue tiers if health flags arise.

Lemonade: Term life only, up to $1.5M (direct digital cap). Fully automated, no physical exam. Not available in NY.

Bestow: Term life only, up to $3M. Strictly algorithmic underwriting with instant data checks; no physical exam fallback.

Coverage recommendation: As a rule of thumb, target 10-20x annual income, adjusted for debts, childcare, and college goals. Buy level term while you’re young and healthy. Tax treatment: Premiums not tax-deductible (purchased with after-tax dollars). Considerations: Get coverage now while young and healthy. Waiting means higher premiums or potential decline.

Considerations: Get coverage now while young and healthy. Waiting means higher premiums or potential decline.

Estate Planning

Estate planning specifies what happens to your assets and accounts if something happens to you. For a newborn: who’s the guardian, who manages finances, what happens to each account, how it all connects. Without a will or trust, state law decides who raises your kid and manages their money. With one, you decide.

The players:

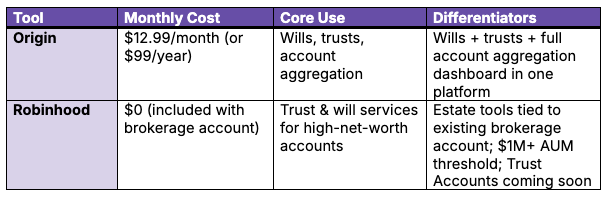

Origin: A platform for trust/will creation and comprehensive financial dashboard. Users can specify guardians, set up trusts, and access a centralized dashboard for all accounts (checking, savings, 529s, investments, insurance) in one place. I found this process to be seamless and a great add-on to an already useful PFM tool.

Robinhood: Offers trust and will services (Robinhood Concierge, via Vanilla Technologies) for accounts with $1M+ in assets, plus a separately rolling out Trust Accounts brokerage feature for lower balances.

Considerations: Update documents every 3-5 years as circumstances change. Your priorities at birth differ from those at 10. Make beneficiary designations and contingent guardians consistent across accounts and documents.

Fintech is Everywhere

Here’s what’s clear: I can map out this entire financial infrastructure for a human who can’t hold their head up yet - using multiple fintech platforms, and a half-dozen tax-advantaged account types. I only wish there was a centralized dashboard for all of this, but Origin does get me pretty close.

A decade ago, this required a financial advisor, a CPA, a stack of paperwork, and months of coordination. Now it’s componentized and plug-and-play. The pieces snap together. And that changes what’s achievable for ordinary families.

Not just neobanks and payments. Not just investing apps. But tools that structure financial life from birth to retirement, for humans who can’t speak yet.

Fintech is everywhere. Even in the nursery.