Wells Forgo-ing The Bilt Deal Was Not On My Bingo Card

But it's not the economics that doomed this partnership like they want you to think

Yeah, this was awkward. The same day I posted about Wells Fargo's deal, Bilt announced a $250M round valuing the firm at $11B with $100M of strategic capital from United Wholesale Mortgage and WF is ending the deal early. Was I off the mark?

Maybe it wasn’t actually about economics.

The early termination of the Wells Fargo deal initially confused me. I still firmly believe that economically this wasn’t a bad deal for Wells Fargo, especially since the core criticisms came from a WSJ article that misinterpreted Wells Fargo executives’ statements. One example of many I detailed in my post:

WSJ said Wells Fargo assumed 50-75% of balances would be revolving. However, for the credit score Bilt targeted, the revolving balance is only 20-30% or less. Given the size of an average rent payment in someone’s monthly spend, getting to 50-75% would mean targeting subprime creditors (which aren’t eligible for the card at <580) OR assuming the core demo can revolve on rent payments (which isn’t possible or this product wouldn’t exist).

Instead, Wells Fargo likely assumed 50-75% of non-rent payments would revolve, amounting to ~10-15% of total balances. This assumption aligned with the actual metrics from the partnership, indicating the deal wasn’t unexpected economically. There’s unfortunately a few other misinterpretations in the article like this which when reinterpreted make it clear that the partnership economics were actually sound.

But on a basic level, Wells Fargo also acquired ~675K cardholders for ~$120M/year. If you're a bank, you'd pay $180 CAC any day since customer acquisition is often $1K+ given the average bank relationship lifetime is 10+ years. Remember Chase CEO Jamie Dimon's quote:

One of the fictions here is that the marketing cost ... gets booked over 12 months. The benefit of the card gets booked over 7 years. The card was so successful it cost us $200 million, but we expect that to have a good return on it. I wish it was a $400 million loss.

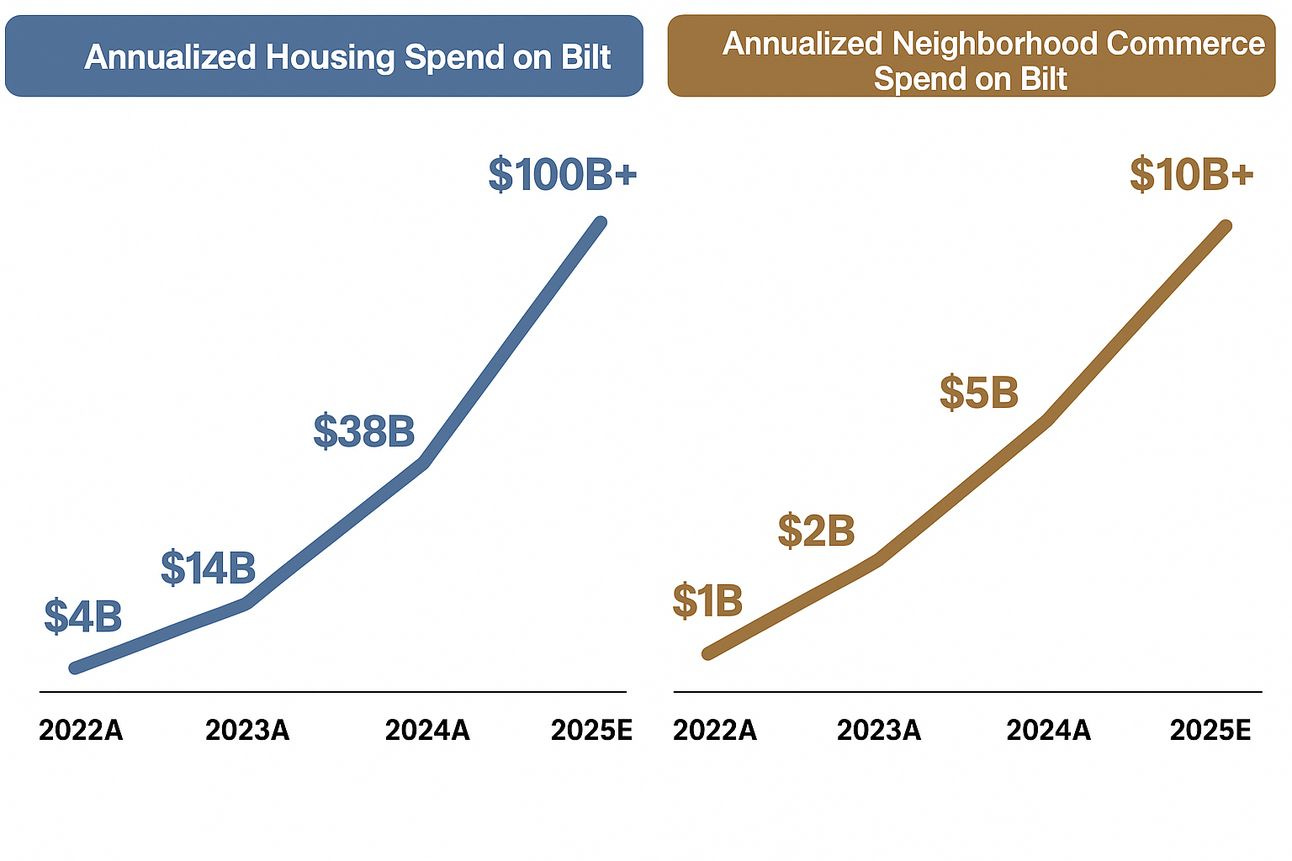

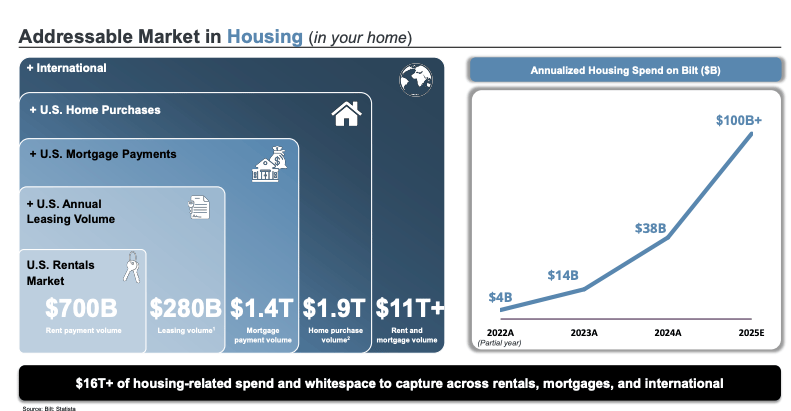

Of course, the business model was potentially different than what Wells Fargo imagined when it underwrote the deal. Even this is a stretch because the numbers show card spend was never more than ~25% of overall rent payments and rapidly went down so it couldn’t have been a surprise. In any case, with $1.4B in outstanding balances per WSJ, and ~675K members (15% of 4.5M homes on the platform), the $2K average revolve might not have looked appealing from a traditional credit card economics standpoint, but it was about much more.

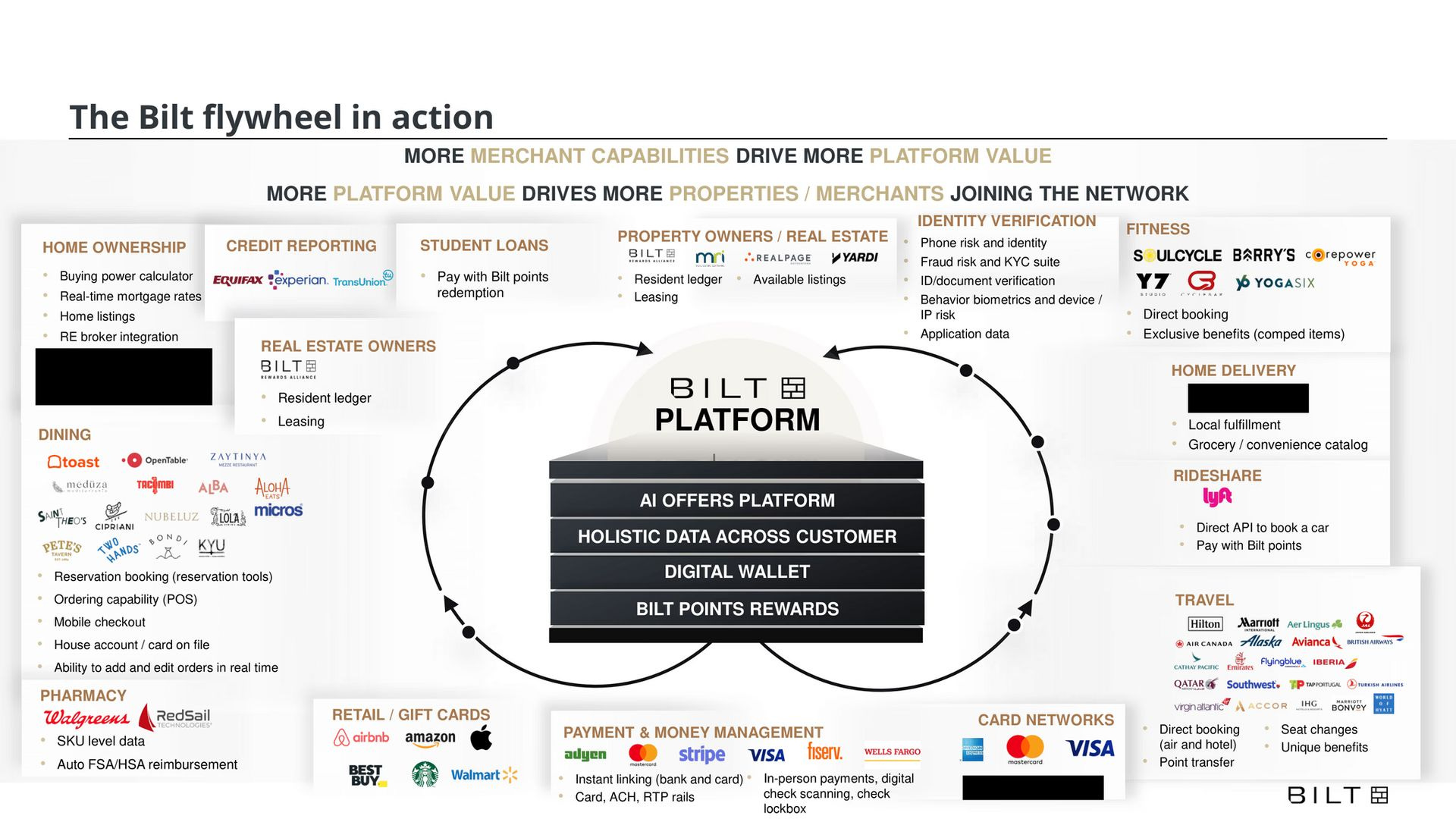

Instead of a card with high revolving balances and a traditional credit card economics model, they were getting a customer acquisition engine and a lower-touch, lower brand engagement sponsor bank model. While Wells Fargo could have run a sponsorship model that many banks have minted billions with, it wasn’t ready to take on this model that Cardless, Bilt’s new card partner and behind Coinbase’s new Bitcoin Amex card, will now monetize. The economics are viable, but some banks must be ready to take a less prominent role if they can't bring the rewards network.

The banks that power your favorite fintechs

posts.interspace.ventures/p/the-banks-that-power-your-favorite

But Wells Fargo wanted to increase their brand equity. They wanted what Chase got with Chase Sapphire Reserve - the Wells Fargo Bilt Card. Instead, it became the Bilt Rewards Card with a tiny Wells Fargo reference. That's Wells Fargo's loss and an opportunity for First Electronic Bank, the sponsor bank powering Cardless.

Don’t be surprised by more new entrants in this space. When valuations reach decacorn status, startups will emerge. I see potential entry points from one or all of the following:

Chase entering directly and leveraging its in-house and partnerships-driven rewards network or issuing via a co-brand.

Amex (with its substantial Offers rewards platform) entering via co-brand partnership to launch this partnership, potentially issuing through Cardless or Imprint.

A startup partners with either to issue a “points on rent + points on mortgage” card. Haven, Mesa and Further are already in the mix. It’s going to grow.

It’s a great time to enter the space Bilt has paved, given the expected expansion into condos & HOAs, student housing, and mortgages. It’s a different model, but one that can work well; consider the co-brand cards from Chase or Capital One.

Share this post from Interspace

Maybe it was a technology and CX problem.

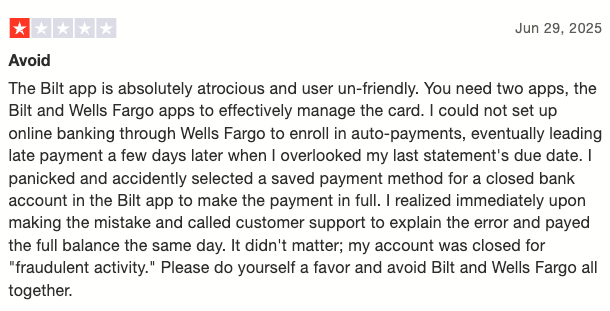

Of course, to be the bank behind the fintech, you need to be built to engage with a tech-forward company and a tech-savvy userbase. It’s unclear if Wells Fargo was ready for this experience. Its underlying technology and integrations were a sore spot for Bilt with complaints about customer support and card repayments leading to a low 1.7/5.0 rating on Trustpilot:

Bilt would have wanted to disintermediate Wells to improve the customer experience, but this would have made it harder to identify Wells Fargo behind the app. Given Wells Fargo’s regulation, it likely made sense to reduce and retrench the business rather than overhaul the legacy tech infrastructure.

Maybe it was fear of competition.

While Wells Fargo let people believe the end of the deal was an economics story, it was probably bristling at Bilt signing up another mortgage provider, United Wholesale Mortgage, which invested $100M of strategic capital into the latest round.

United Wholesale Mortgage (UWM) is a wholesale mortgage lender that underwrites loans for independent real estate brokers. Since 1986, UWM has been the largest mortgage lender in the U.S. Brokers originate loans for home buying, and UWM underwrites and funds them, then sells them to secondary markets of mortgage servicers. They also provide tech, training, and support for mortgage brokers.

Bilt was always going to build a marketplace because multiple providers make a network compelling. But if WF had to compete on price, they knew they wouldn't always win. Perhaps it was better to exit the partnership rather than becoming commoditized in a race to the bottom on pricing.

The breakup was better for everyone involved. Bilt gets a tech-forward partner that doesn’t mind taking a backseat on brand because it monetizes on transaction volume and deposits, not customer acquisition and cross-sell. Bilt adds UWM to supercharge its mortgage and home-related services expansion while Wells Fargo rethinks its strategy.

If you Bilt it, they will come (with high-flying valuations)

Finally, a word on Bilt's valuation. I assigned a lofty 15x multiple on $200M of revenue. Should the valuation be $15B when the company reaches $1B in NTM revenue? No, not when it is operating what will be primarily a rewards network at mature scale with more measured growth prospects.

An excellent article from my friend Michael Bloch, Partner at Quiet Capital, states that Delta made ~10% of its revenue (almost $6B in absolute and up to 50% of its profits) from co-brand partnership with Amex, a useful proxy for Bilt's rewards network business model.

Let's assign a generous $20B to the Delta rewards network with Delta's market cap of ~$40B. That gives rewards a 4x multiple. So what does that mean for Bilt, who is expecting $1B in revenue by Q1 2026? That takes us back to ~$4B for Bilt. Back in my day, $4B was impressive though, but maybe not good enough for Bilt's lofty aspirations.

Let’s see how Bilt’s valuation develops as it matures into a potential IPO-ready company in a few years. Perhaps Bilt’s high-flying valuation will be a rising tide to lift all boats, or maybe we’ll see the true valuation rationalize with time.